Investing in Mutual Fund And Gold Asset Explained

Discover the benefits of investing in mutual fund gold asset. Learn how mutual fund schemes tracking gold prices can be a smarter alternative to buying physical gold, like jewellery. Make informed decisions on your gold investments today!

FINANCE & ECONOMICS

Gold Asset

Investing in Mutual Fund Gold Asset means we are putting our money in a scheme that tracks the price of gold instead of us buying physical gold like jewellery.

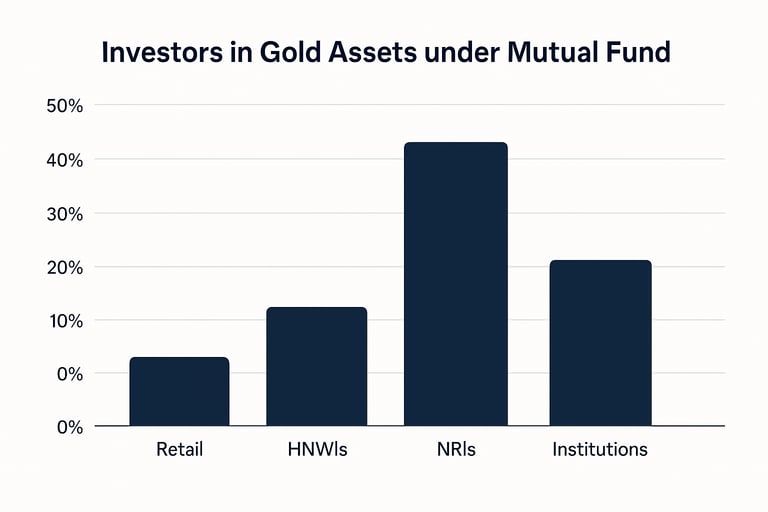

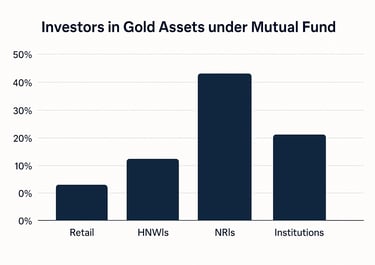

A comparison chart showing Investment percentage in Gold Asset

Courtesy: Youtube Channel @morningmoneybuzz

Gold Mutual Fund : Types

1. Gold ETFs (Exchange Traded Funds)

When we invest our money in Gold ETFs Mutual Fund, Fund Managers invest our money in physical gold (99.5 % purity). These are traded on the stock exchange market, just like shares. They directly track gold price. It requires a Demat Account.

2. Fund Of Funds (FOF)

A Gold Mutual Fund (FOF) is a mutual fund scheme that invests in Gold ETFs not directly in physical gold. We invest in FOF. They invest in Gold ETFS. Gold ETFS invest in physical gold. We don’t need any Demat account or buying physical gold. These are managed by professional fund manager through an AMC (Asset Management Company).

Some names of Asset Management Company

AXIS Mutual Fund, HDFC AMC, ICICI Prudential, Kotak Mutual Fund and SBI Mutual Fund.

These Gold Mutual Fund doesn’t pay dividends or interest. Return or profit comes from only capital appreciation (increase in NAV).

3. Gold Mining Funds or International Gold Funds

A gold Mutual fund where investments are made towards Stocks of Gold Mining Companies and not in gold itself. Mutual Fund invest in the stocks of gold mining companies. These companies deal with exploring,mining, processing and refining of gold.

In this type of Gold Mutual Funds, the returns depend on profit of mining company, company efficiency at operation and debt i.e. company performance. The other factors that decide the returns are Stock Market Fluctuations and Currency Exchange Rates.

Describing With Example

Returns from investing in Gold ETFs

1. The Investment in Gold ETFs require us to invest in Lump sum amount and not through any SIP.

We require a Demat Account as told earlier. Say we invest Rs 5000/- in lump sum amount to Gold ETFs for 2 years. When we invest that is initial NAV was Rs 50/- per unit. So total units bought as per formula that is

Total Investment / Price per unit. Which is equals to 5000/50 = 100 units.

After 2 years NAV value increases due to Gold Price Movements to Rs 70 per unit. So, after 2 years Total Investment amount will be 100 x 70 which is Rs 7000/-. Our total Profit from investment is Rs 7000 – Rs 5000 = Rs 2000/-. Investment options are possible only manually not automatically like in Equity and Bond Asset.

Returns from investing in Gold (FOF)

2. The Investment in Gold FOF can be done through SIP or Lump sum without needing a Demat Account.

We invest Rs 5000/- every month in Gold Mutual Fund. We start the SIP in January for 5 months The Gold Mutual Fund will track the price of Gold through a Gold ETF. Total duration of investment is 12 months. When we invest that is initial NAV was Rs 50/- per unit. So total units bought as per formula that is

Total Investment / Price per unit. Which is equals to 5000/50 = 100 units

Say from January to May we invest Rs 5000/- every month. So, our total investment = Rs 25000/-

January: Rs invested 5000/- NAV price per unit Rs 50/- then units bought is 100

February: Rs invested 5000/- NAV price per unit Rs 52 then units bought 96.15

March: Rs invested 5000/- NAV price per unit Rs 48 then units bought 104.16

April: Rs invested 5000/- NAV price per unit Rs 51 then units bought 98.03

May: Rs invested 5000/- NAV price per unit Rs 53 then units bought 94.33

Total Unit = 492.67 (100+96.15+104.16+98.03+94.33)

Now say after 12 months NAV unit price is Rs 56 so now the unit we hold will have a value of Rs 27,589.52 (492.67 units multiplied by Rs 56). So, Capital gain is Rs 2,589.52 (Rs27,589.52 - Rs25000). We can redeem this value in cash anytime by selling the NAV units.

Returns from Investing in Gold Mining Funds

3. There are 100 investors each investing Rs 100000/- (1Lakh). So Total Asset sums up to Rs 10000000/- (1Cr). So total investment is 1 cr.

And NAV unit price was Rs 10 per unit. So total unit issues were

Total Investment / Price per unit

= 10,00,000 units

• Fund Managers diversify these investors fund at different interest rates for Gold Mining Company asset of mutual fund as follows

• 25 lakhs in Newmont Corp, 20 lakhs in Barrick Gold, 15lakhs in AngloGold, 20 lakhs in Franco Nevada and 20 lakhs in Wheaton Precious.

Weighted average return = (25% x 9%) + (20% x 8%) + (15% x 6.5 %) + (20% x 10%) + (20% x 9%) = 8.5% approx.

Here diversification is done among companies and regions but the entire theme is still Gold Mining not as diversified as a regular Equity Mutual Fund.

• Total Asset of the fund before expense or Annual Return from Gold Mining Company Asset Investment by Mutual Fund companies as follows.

Total Asset of the funds before expense 8.5% of 10000000/- = Rs 850,000/-

Liability Cost is charged as 1 % by mutual fund company.

Total Liability Cost = 1% of 10000000 = 100000 /- i.e. (1 lakh)

Total Fund = (Total Asset – Total Liability)

= (850000 – 100000)

= 750,000/-

• NAV growth rate for 5 year is reflected as 7.5% (Since the net return after expense is 7.5%). Initial NAV was Rs 10 per unit and after 5 years it grows at 7.5 % yearly at compound interest rate and now the final or new NAV is

= 10 (1+ 7.5%) ^5

14.35 per unit

• Total Units Issued were 1000000 and Total Investors were 100 so each investor holding 10,000 units.

Now after 5 Years value per investors is

= 10,000 x 14.35

= 1,43 ,500/-

So total Fund Value after 5 Years increases from 1cr to 1.435 Cr.

i.e. Rs 1,43,50,000/-

The Mutual Fund are investing 1Cr of the investor’s money in Gold Mining Company Asset then earning at 8.5% (Combined) interest rate for 5 years. So, these incomes together paying 8.5 lakh per year for 5 years which sums up to Rs 8.5lakh x 5 which is 42.5 lakhs. So, in total they are returning the principal amount of 1 Cr along with 42.5 lakh interest for 5 years. So Mutual Fund Company are getting 1.425 Cr as return to their investment.

But the Mutual giving its investors 1.435Cr and not 1.425Cr because

Gold Mining Company Assets pay in simple interest 8.5% yearly but Mutual Fund also reinvest yearly interest compounding the returns internally (after deducting expenses) that’s why NAV grows faster than simple interest. So, in this example mutual fund grows more than 1.425 Cr and reached 1.435Cr.

Although the Mutual Fund getting less interest amount after 5 years from rental income as the Gold Mining Assets paid in Simple Interest and not in compound interest. What Mutual Fund Companies do is that they reinvest this 8.5 Lakh incomes on new Gold Mining Company Assets every year at same 8.5% return.

If calculated after 5 years then Mutual Fund Company earning Rs 1,50,36,067 i.e. Rs1.5036 Cr from 1.425cr (calculated earlier).

Mutual Fund Companies earning from interest income is Rs 1,42,50,000 /-.

Fund Managers reinvest this amount for 5 years at same interest to earn Rs 1,50,36,067/-.

Finally, they are giving Rs 1,43,50,000/- to the investors.

Facts to Remember

1. Gold Price Movement: If international or Indian Gold price rises then NAV rises and vice versa

2. Currency Exchange: Gold is priced globally in US dollars. If Rupee weakens vs USD then NAV goes up. If rupee strengthens NAV can go down.

3. Liability Cost: The fund deducts annual expenses which slightly reduces NAV growth.