Investing in Mutual Fund and Bond Asset Explained

Discover how investing in mutual funds can help you grow your money through bonds. Learn about the interest earned from these debt instruments and the return of your principal at maturity. Explore the benefits of mutual fund investments today!

FINANCE & ECONOMICS

Describing Bond Asset

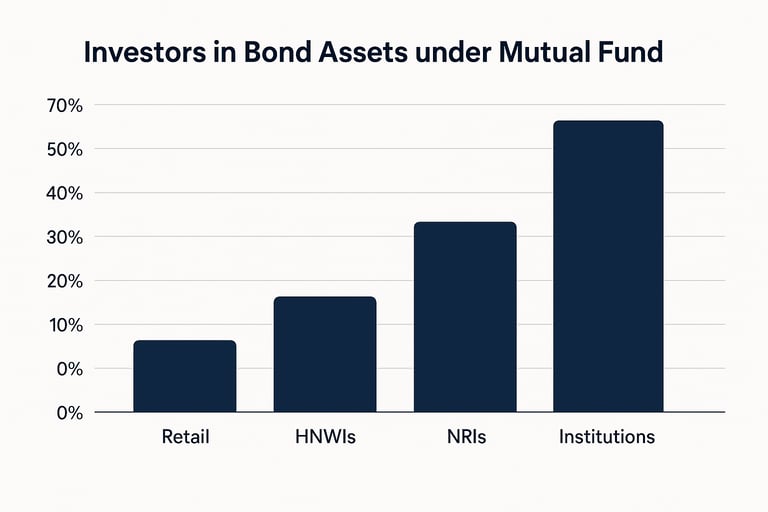

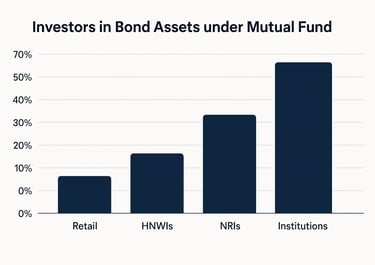

Comparison Chart Showing investment percentage in bond asset

When we invest our money in mutual fund and they in turn invest that money to the government, companies and institutions called debt instruments (bonds) that looks like lending. In return they pay you interest called coupon regularly and also return your principal at the end of a fixed term called maturity date.

Describing in Details

Here the bond issuer needs money. The Bond Assets issuer are sometimes banks or companies. they issue bonds in return they promise to pay interest with principal amount in future.

The Fund managers on behalf of Mutual Fund buys those bonds with investor’s money. so Mutual fund is somehow lending the money to the issuer.

The issuer gives regular interest income called a coupon to the Mutual Fund. And principal repayment on maturity. These earnings (interest + Maturity amount) go into Mutual Funds total earning. which are reflected in NAV or even paid as dividends to investors.

Courtesy: Youtube Channel @morningmoneybuzz

Type of Bonds Mutual Fund Invest

1.Government Bonds (G-Secs): Issued by Indian Government

2. AAA Corporate Bonds : Issued by large private firms (Reliance)

3. AA Corporate Bonds : Issued by large companies (L& T)

4. Debentures: Issued by Companies

5. T-Bills : Issued by government (Short term)

6. State Government Bonds (SDLs): Issued by State Governments

7. Inflation -Indexed Bonds: Issued by RBI/ Governments.

Describing With Example

1. There are 100 investors each investing Rs 100000/- (1Lakh). So Total Asset sums up to Rs 10000000/- (1Cr). So total investment is 1 cr.

And NAV unit price was Rs 10 per unit. So total unit issues were

Total Investment / Price per unit

= 10,00,000 units.

2. There are many companies Private and Government institutions. Who issue Bonds. They are issuing Bonds for 5 years at different interest rate(coupon) per year in return for funds.

3. Now the Mutual Fund invest in those Bond Assets issued by the companies or government institution. They lend Rs 1 crore to buy those bonds.

4. Fund Managers diversify these investors fund under Bond asset of mutual fund as follows

5. 40 lakhs in Government Securities, 30 lakhs in AAA Corporate Bond, 20 lakhs in AA Corporate Bond and 10 lakhs in state Government Bonds.

Weighted avg return:( 40% x 7%) +( 30% x 9 %) + (20% x 11%) + (10% x 8%) = 8.5 %

6. The Company / Government Institutions pay interest of Rs 8.5lakh/year and after 5 year that is end of maturity period, they repay 1 crore principal amount to the Mutual Fund along with interest amount.

7. Total Asset of the fund before expense or Annual Return from Bond Investment by Mutual Fund companies to the Government and Private institution is as follows.

Total Asset of the funds before expense 8.5% of 10000000/- = Rs 850,000/-

8. Liability Cost is charged as 1 % by mutual fund company.

Total Liability Cost = 1% of 10000000 = 100000 /- i.e. (1 lakh)

Total Fund = (Total Asset – Total Liability)

= (850000 – 100000)

= 750,000/-

9. NAV growth rate for 5 year is reflected as 7.5% (Since the net return after expense is 7.5%). Initial NAV was Rs 10 per unit and after 5 years it grows at 7.5 % yearly at compound interest rate and now the final or New NAV is

= 10 (1+ 7.5%) ^5

14.35 per unit

10. Total Units Issued were 1000000 and Total Investors were 100 so each investor holding 10,000 units.

Now after 5 Years value per investors is

= 10,000 x 14.35

= 1,43 ,500/-

So total Fund Value after 5 Years increases from 1cr to 1.435 Cr. 11. The Government Institutions who are borrowing Rs 1Cr(combined) at a 8.5% (Combined) interest rate for 5 years. So, these institutions together paying 8.5 lakh per year for 5 years which sums up to Rs 8.5lakh x 5 which is 42.5 lakhs. So, in total they are returning the principal amount of 1 Cr along with 42.5 lakh interest for 5 years. So Mutual Fund Company are getting 1.425 Cr as a return to their investment on these debt instruments.

12. But the Mutual giving its investors 1.435Cr and not 1.425Cr.

13. Institutions pays in simple interest 8.5% yearly but Mutual Fund also reinvest yearly interest compounding the returns internally (after deducting expenses) that’s why funds NAV grows faster than simple interest. So, in this example mutual fund grows more than 1.425 Cr and reached 1.435Cr.

14. If calculated after 5 years then Mutual Fund Company earning Rs 1,50,36,067 i.e. 1.5036 Cr from 1.425cr (calculated earlier). Mutual Fund Companies earning from institutions Rs 1,42,50,000 /-. Fund Managers reinvest this amount for 5 years at same interest to earn Rs 1,50,36,067/-. Finally, they are giving Rs 1,43,50,000/- to the investors.

15. Although the Mutual Fund getting less interest amount after 5 years from debtors as the institutions paid in Simple Interest and not in compound interest. What Mutual Fund Companies do is that they reinvest this 8.5 Lakh incomes on new assets every year at same 8.5% return. Its also called Reinvestment of Coupons.

Facts to Remember

The Bond Issuer decides the Interest Rate by keeping in Mind

1. RBI Repo Rate:

The base rate at which bank borrows from RBI. All lending and borrowing in the country get affected by Repo Rate. If Repo rate rises then bond rates also rises

2. Market Interest Rate:

If bank offers 7% interest rate on fixed deposits then investors won’t buy bonds offering only 5%. So, the bond issuers must stay competitive

3. Issuers Credit Rating:

A risky Company must offer high interest rate whereas AAA rated company or a strong government can offer low rates.

4. Inflation Expectations:

If Inflation is expected to rise then bonds must offer higher rates to give real return

5. Maturity Period: Longer the bond, usually higher the interest due to more risk over time.